The Strategy That Always Feels Like It’s Working

Monte Carlo Meets The Martingale Strategy

The martingale is a simple strategy: after a loss, double the bet. After a win, return to the base bet and collect a net profit equal to the original stake. The logic holds in theory. If you can always place one more bet, you will eventually recover every loss.

The only constraint is capital, you simply need an infinite amount of it!

What You’re Watching

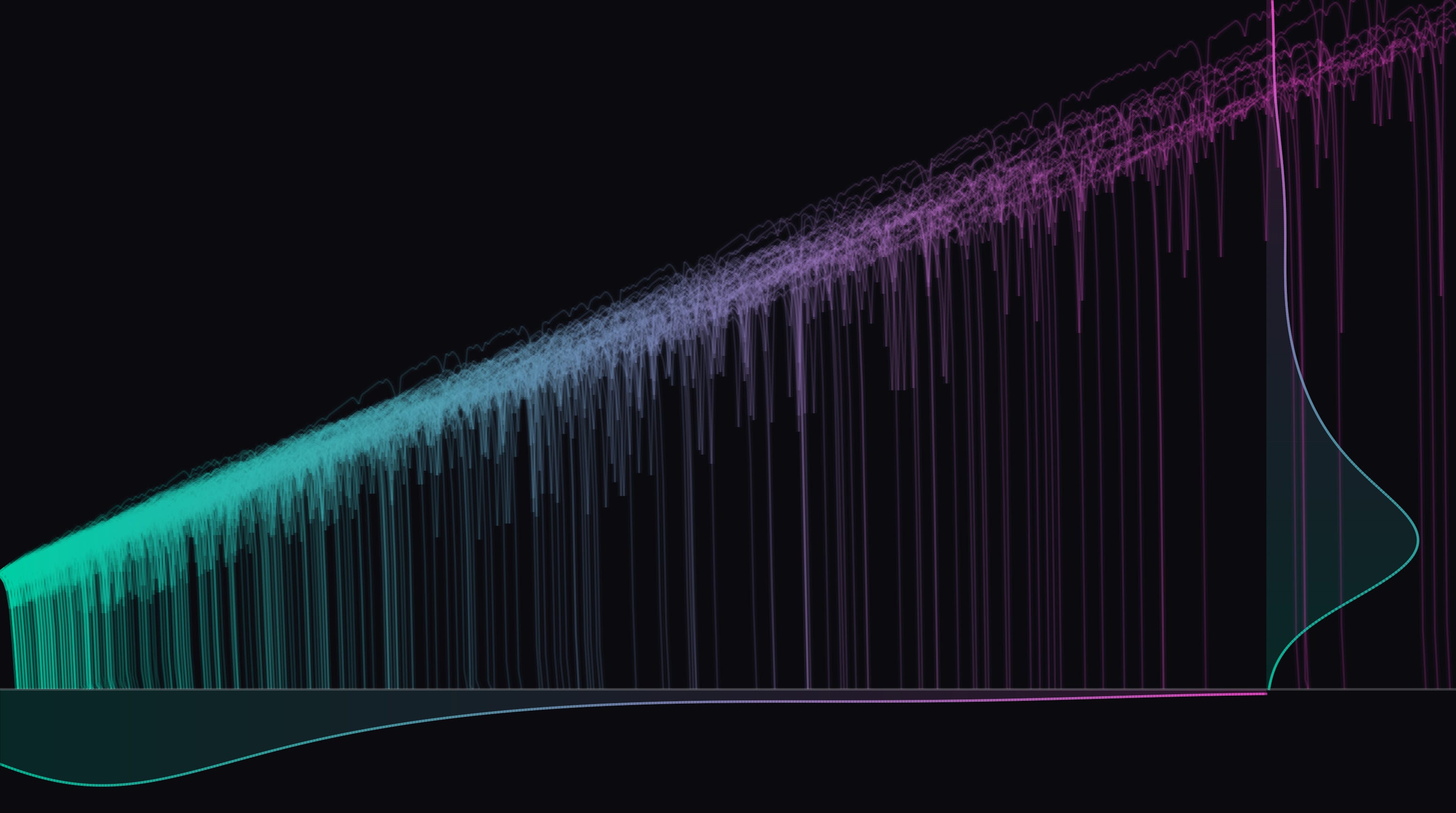

This is a Monte Carlo simulation: 200 independent runs of a martingale strategy applied to a stock modelled by geometric Brownian motion. Each run uses a different random seed, a different sample path through the same underlying market process, so the variation reflects genuine statistical dispersion.

In each run, a bankroll of $1,000 bets on whether the next return is positive or negative. A win collects the stake. A loss doubles the next bet. A subsequent win resets the bet to the base and continues.

The line draws forward. Sometimes it climbs for a long time. Then it falls to zero, fades out, and a new attempt begins from scratch with the same strategy and fresh capital on a different random path.

All 200 attempts end at $0.

Two distributions build up in the margins as the paths accumulate. The bottom shows when ruin happens (time-to-ruin). The right shows how high the bankroll reached before the collapse (peak equity). Across 200 runs:

The time-to-ruin distribution is heavily right-skewed: half the runs are finished by step 64, well below the mean of 133. The peak equity distribution shows that many paths barely move before collapsing, though a meaningful tail reaches $5,000 or more. The strategy produces real gains over extended periods before ruin arrives.

The Exponential Trap

Starting at a base bet of $20, a losing streak produces the following sequence:

Six consecutive losses on a $1,000 bankroll leave the required next bet at $1,280, exhausting the capital:

If you’re not convinced, please pay attention to the following:

Stocks fall roughly 46% of trading days, so any given day is close to a coin flip going against you. Six consecutive losses have a probability of 0.466 ≈ 1%, or about 1-in-100.

That appears small in isolation. But consider how many opportunities exist for it to occur within a single run:

A 1,000-step sequence contains windows starting at step 1, step 2, step 3, and so on up to step 995, each one a fresh candidate for a six-day losing streak. That is 995 independent chances for the ruin condition to be triggered.

The probability that none of them produce a streak is 0.99995, which is close to zero. Hence, the probability that at least one does is close to 1−0.99995 ≈ 100%.

In English, the martingale strategy has 100% chance to bankrupt you. It is simply a matter of when, and as seen in the animation above, the Time-to-Ruin distribution peaks very close to the start, meaning you will go bankrupt sooner than later.

The Market Has No Memory (In This Model)

The martingale implicitly assumes that a long losing streak raises the probability of a win. After five consecutive down days, the reasoning goes, the sixth should go up.

The simulation here uses geometric Brownian motion, where returns are drawn independently at each step. Under that assumption, prior losses carry no predictive weight for what comes next, and the streak-reversal logic the martingale relies on simply does not hold.

Real markets are more complicated. Volatility clustering, momentum effects, and other empirical regularities mean returns are not strictly independent in practice. Whether those dependencies are large enough, stable enough, or tradeable enough to save the martingale is a separate question. Even if returns do tend to reverse after a losing streak, the strategy only survives if that reversal arrives before the bankroll runs out. Each additional loss doubles the next required bet, so the remaining time to wait for a recovery shrinks with every step deeper into the streak.

Given infinite capital and infinite time, the strategy would eventually recover every loss under almost any return process. Capital is finite, and the required bet sizes grow faster than any realistic edge could offset.

The Peak That Never Holds

Many paths in the animation reach substantial highs before collapsing. Gains that accumulate over 200 or 300 steps would appear as strong performance on any periodic statement. The martingale can produce extended winning periods because the base bet is small relative to the bankroll at the start.

The structure of every collapse is the same. The final losing bet is also the largest bet ever placed by that path. The strategy is designed to swing largest precisely when the bankroll is most stressed, after a run of consecutive losses. The profitable periods are part of how the strategy operates, not evidence that ruin is avoidable.

What This Means

The martingale conflates sequence with edge. Managing the sequence of bets in response to losses creates the appearance of risk control while the underlying exposure grows exponentially.

Position sizing matters as much as direction. Increasing bet size after losses, whether labelled as doubling down, averaging down, or adding conviction, amplifies exposure at the point of maximum drawdown. The terminology varies; the sizing follows the same exponential curve in every case.

The Kelly Criterion defines the maximum fraction of capital to bet for long-run survival. The martingale inverts that logic by committing more capital precisely when the position is already losing, accelerating toward the worst outcome the longer it continues.

The 200 paths above use the same model and the same parameters across different random seeds. Each path looks different, but each one ends the same way.

Simulation: GBM with μ = 3%, σ = 22% annualized, dt = 1/252. Starting capital $1,000. Base bet $20. Bet doubles after each loss, resets after each win. Ruin declared when required next bet exceeds remaining capital. 200 independent paths, each using a distinct random seed. Bottom margin shows the distribution of time-to-ruin; right margin shows the distribution of peak equity before ruin.