Size Matters: The Kelly Criterion

Why overbetting mathematically ruins you

What You’re Watching

The animation shows a biased coin — 60% heads, 40% tails. Both players start with $100 and bet on every single flip. They see the same sequence of outcomes. The only thing that differs is how much they bet each round.

The Overbettor (red) bets 50% of their bankroll every flip. It seems reasonable — the coin favors you, why not bet big?

The Kelly Bettor (teal) bets 20% of their bankroll every flip — more conservative.

The first 25 flips play out slowly. Both players win some, lose some. The overbettor looks competitive — sometimes even ahead. Then the animation fast-forwards to flip 200.

The result is very different.

The Formula Behind the 20%

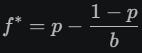

The Kelly Criterion gives you the exact fraction of your bankroll to bet in order to maximize the long-run growth of your wealth.

For a simple win/loss bet with probability p of winning and b-to-1 payoff:

If a bet has a 60% chance of winning (p=0.6) and 40% chance of losing (q=0.4), and the bet pays 1-to-1 (b=1):

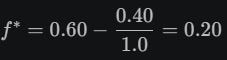

That’s it, 20%. Bet more than that and your growth rate falls below its peak. Bet more than twice that — above 40% — and you are guaranteed to destroy your bankroll over time. The overbettor, betting 50%, is already past that point:

Why Overbetting Ruins You

This is the unintuitive part. The overbettor isn’t unlucky. They’re wrong in expectation.

Each flip, the overbettor at f=0.50 multiplies their wealth by:

Over many flips, the geometric average per flip is:

Less than 1. Every flip, on average, they lose 3.3% (0.9667-1) of their bankroll. The positive expected value of each bet is real but it’s an arithmetic illusion. That’s because wealth compounds geometrically. And geometrically, they’re bleeding out with every coin toss.

The Kelly bettor at f=0.20 computes to:

Each flip adds 2% (1.02 - 1) in geometric expectation, which over 200 flips starts doing some seriously compounding.

What This Means in Practice

The Kelly formula is a ceiling, not a target. Betting the full Kelly fraction maximizes long-run growth but produces brutal volatility along the way and drawdowns of 50%+ are common. Most professional gamblers and traders use a fractional Kelly (half or quarter Kelly) to smooth the ride, accepting somewhat lower growth in exchange for much less variance.

Every bet you make has an implicit fraction. If you own a stock position, that position is a fraction of your total wealth. If you’re sizing positions by gut feel, you are implicitly running some bet fraction — almost certainly not the one that maximizes your long-run outcome.

The math is symmetric. Kelly doesn’t just tell you how much to bet when you have an edge. It also tells you: if you have no edge, the optimal bet size is zero. Playing a fair or unfavorable game longer does not help you. Only positive-expectation opportunities deserve capital.

This is why the house always wins. Casino games are slightly negative expectation. That means the Kelly-optimal fraction is negative — you should be on the other side of the trade. Over time, any bettor who keeps playing a game with negative edge will converge to ruin, no matter how clever their system.

Simulation: 200 coin flips, p=0.60 heads probability, b=1.0 payoff ratio, starting bankroll $100. Overbettor: f=0.50. Kelly Bettor: f=p−(1−p)/b=0.20. Both players see the same flip sequence (seed 42).